Business Aircraft: Buying New or Used?

Choosing the option that’s best for you (Part 3 of 3)

Back to Articles

David Wyndham

David Wyndham has extensive expertise in aircraft sales and acquisitions, asset management, cost and...

Having addressed advantages for buying new and pre-owned aircraft, David Wyndham concludes his series of pivotal considerations for Boards looking to acquire business aircraft…

Previously, we touched on only two aspects of the new vs. pre-owned question: acquisition cost and operating costs. While those are two significant areas in arriving at a purchase decision, we always recommend looking at the full life-cycle cost of owning and operating the aircraft.

Some fixed costs such as crew salaries, hangar and liability insurance may be unrelated to the new vs pre-owned question. But what about financing the acquisition? Are there more favorable terms for new aircraft? What about residual value of the aircraft at the end of your ownership? For business use, taxes and tax depreciation are also important.

Financing

When looking at the costs to acquire, operate and dispose of the aircraft, used aircraft can often have a significant cash advantage. Consider the new and five-year old mid-sized business jets we used as illustrative in Parts 1 and 2 of this series as an example. Highlighted in Table A is the total cash outlay calculated for a five year ownership period.

Financial institutions do not mind taking a residual value risk on an aircraft that is five or ten years old at the end of the lease or finance term. They are much more wary of 20-year and older aircraft, however. For a new business aircraft, 100% financing at low single-digit rates are available for the best credit risks. Older aircraft tend to require 20% to as much as 50% down-payment to secure financing.

Lease rates and terms also favor the new business aircraft: a 10-year lease on a new business jet is not a problem, while the bank may baulk at longer than five years for a 15-years old business jet.

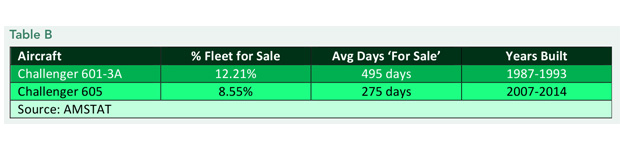

This fact of financing recognizes that selling a newer aircraft in excellent condition is easier than selling a much older aircraft, even when it is in very good condition. As one example, according to AMSTAT, older Challenger 601-3A models for sale take longer to sell than their new variant, the model 605 (see Table B). In general, newer aircraft sell quicker than their older brethren.

Tax Depreciation can narrow the new-versus-used price gap. But the tax advantages are greatest for the first-time buyer of the new aircraft. How? If the aircraft is 100% used for business, 100% of the acquisition price can be depreciated as a business expense. The US Internal Revenue Service (IRS) allows full depreciation in as little as five years for non-commercial operators.

Depending on the tax law and whether you can qualify, there has also been a 50% bonus depreciation law that allows up to half the purchase price to be taken in the first year of use for the aircraft. That feature is not available for pre-owned aircraft.

So the tax depreciation in the first year of service may allow for a $13.3 million deduction for our new aircraft example (see Table C). The used aircraft does not qualify for other than the standard IRS allowance. Note: accelerated depreciation only changes the timing of depreciation, not the duration or amount of total depreciation.

At a 35% tax rate, the new aircraft with bonus depreciation can have a tax advantage of $3,745,000 ($10.7 million depreciation difference at 35% rate).

There are two options when you sell, depending on your subsequent actions regarding aircraft ownership. There will be a capital gains tax on the difference between the sale price and the depreciated value of the aircraft that can negate a significant part of the early deduction.

In order to avoid having a capital gains tax on the aircraft sale price less depreciated value, you may be able to defer the gains tax with a 1031 Like Kind Exchange. But in deferring this gain, the basis of the next aircraft you purchase will carry the impact of the depreciated amount, thereby making you unable to depreciate the full value of the replacement aircraft. This can get quite complicated and requires the advice of a tax expert.

The huge depreciation advantage of the new aircraft is really only useful in the initial purchase year; its value lessens over time. Tax planning overseen by a person knowledgeable in the ways of the IRS is required.

Returning to Table A and assuming 100% business use and a 35% tax rate, the pre-owned aircraft has a net after-tax advantage. This benefit, however, may not always hold true. That is why we always recommend looking at the life-cycle costs for each option. Taxes and financing/leasing options may favor one option under particular circumstances.

In summary, new versus pre-owned aircraft should take into account mission requirements, aircraft capability, owner preferences and life-cycle costs. It can be complicated, so having a consultant's help can make the decision easier. Remember to focus on the objective—safe and efficient transportation using a business aircraft.

Do you have a specific aircraft maintenance, upgrade or repair need?

Use Advantage to outline your maintenance requirements by completing our quick form, and your enquiry will be passed to qualified service providers. Receive the feedback you need to help you choose the right partner and the best deal.Start now

David Wyndham

David Wyndham has extensive expertise in aircraft sales and acquisitions, asset management, cost and budget analysis and finance fundamentals. With several decades supporting aircraft owners and operators in making fully-informed decisions about their aircraft needs, his expertise spans from the flight department to the executive boardroom.

David is the founder of David Wyndham + Associates, and previously he was a Co-owner and President of Conklin & de Decker where he consulted with large corporations, individuals, and government agencies on their aircraft needs.

{kind=link}

{kind=link}

{kind=link}